THE 60-SECOND VERSION

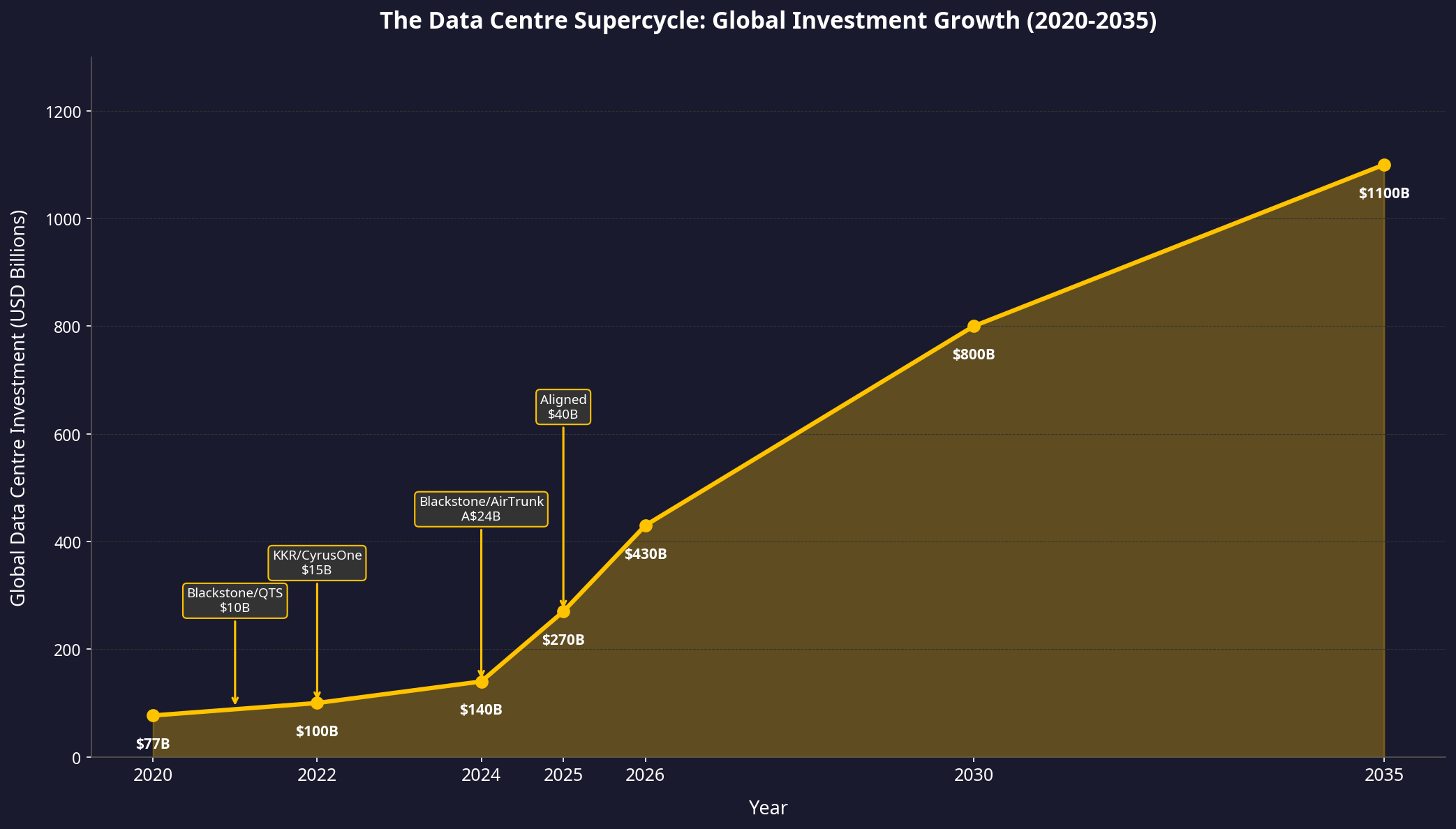

Data centres have gone from a niche corner of the telecoms market to one of the most sought-after asset classes on the planet. Global data centre investment exceeded $270 billion in 2025 alone, capturing more than a fifth of all greenfield foreign direct investment worldwide.[1] We are in the early stages of what JLL calls a $3 trillion infrastructure investment supercycle, with global capacity expected to double by 2030. The tenants are the most creditworthy companies on earth — Microsoft, Amazon, Google — signing long-term leases that generate stable, inflation-linked cash flows. Blackstone’s $10 billion acquisition of QTS in 2021 became the single largest driver of returns across its entire $1.3 trillion portfolio in 2025.[2] Macquarie flipped Aligned Data Centers for $40 billion — the largest data centre deal in history.[6] But this is not a one-way bet. Power constraints are throttling growth in key markets. Valuations have reached levels that make seasoned real estate investors nervous. And at least one billionaire developer is warning that the whole thing could end badly.[5]

The investment case is straightforward: every AI model, every cloud application, every streaming service, and every autonomous vehicle needs computing power, and that computing power lives in data centres. The question is not whether data centres will be important — they already are — but whether the current wave of investment will reward investors or drown them. This deep dive will give you everything you need to understand the opportunity, the risks, and the most intelligent ways to get exposure.

SECTION I

What Data Centre Investing Actually Is

At its core, a data centre is a secure, purpose-built facility that houses the computing infrastructure — servers, storage systems, and networking equipment — that powers our digital lives. Think of them as the factories of the 21st century. They don’t produce goods; they produce the processing power and data storage that underpins everything from your email to the most advanced AI models being trained by OpenAI and Google DeepMind.

For decades, data centres were a sleepy, unglamorous asset class. Most were owned and operated by individual companies for their own needs — a bank running its own servers in its own building. The game changed with the rise of cloud computing, which saw companies like Amazon (AWS), Microsoft (Azure), and Google (GCP) build out massive fleets of hyperscale data centres — facilities with 100,000 or more servers — to rent out computing power to the masses. Now, the AI revolution has poured petrol on the fire. Training a single large language model can consume as much electricity as a small town uses in a year, creating unprecedented demand for specialised facilities capable of handling immense power and cooling requirements.

Investing in data centres means buying into the physical layer of this digital transformation. You are not betting on which AI model will win, or which cloud provider will dominate. You are betting on the undeniable fact that all of them will require vast amounts of computing power, housed in highly specialised, mission-critical real estate. It is, in the truest sense, a picks-and-shovels play on the AI gold rush.

“The historic pace of investment taking place in the US to facilitate the development of artificial intelligence, including the design and manufacture of semiconductors, data center construction, and the expansion of power generation, is the key driver of economic growth today.”

— Stephen Schwarzman, Co-founder and Chairman, Blackstone

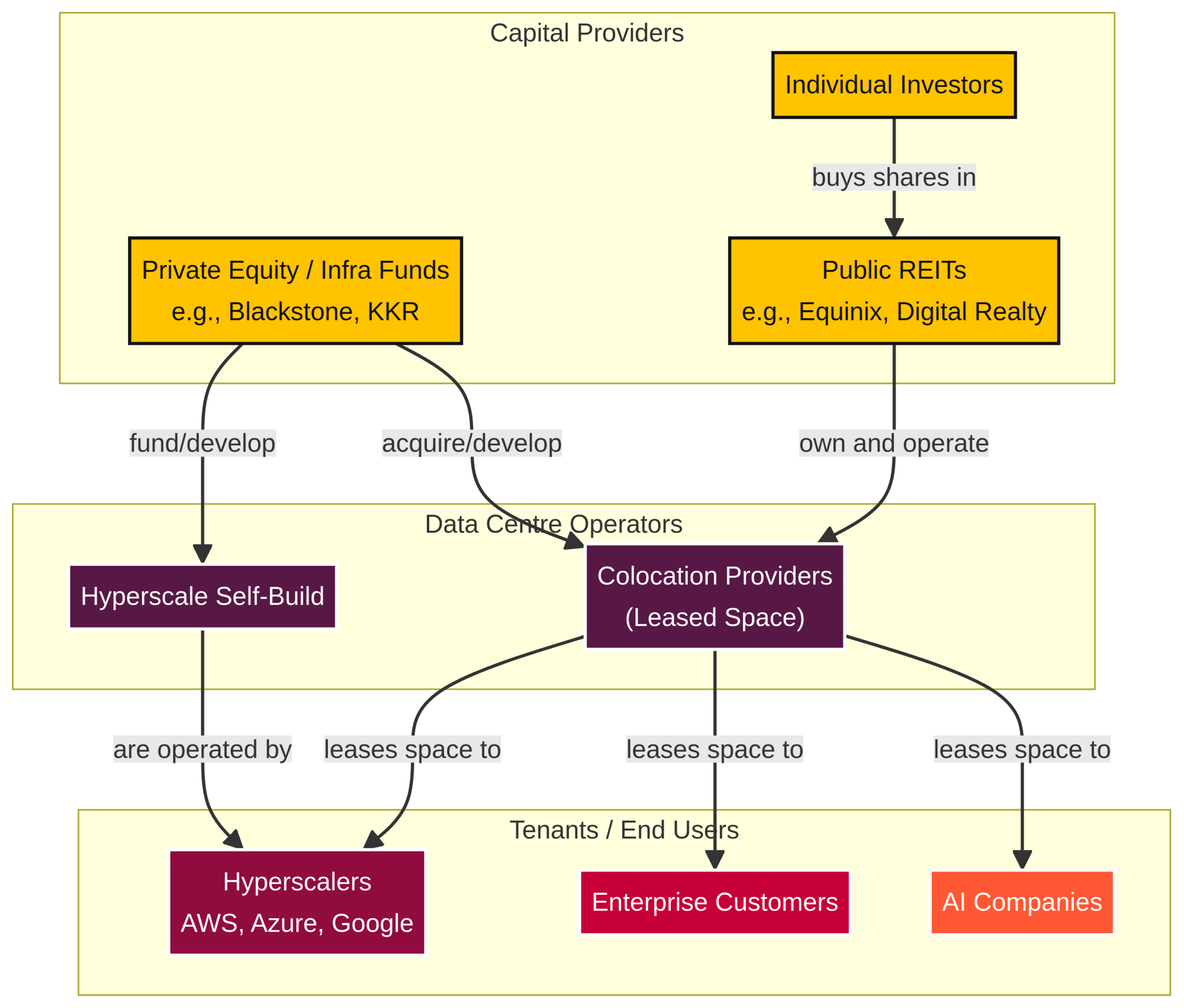

FIGURE 1

The data centre ecosystem — how capital flows from investors through operators to the hyperscaler tenants that generate revenue.

SECTION II

The Market: From Niche Telecom to a $350 Billion Asset Class

The journey of the data centre from a corporate IT closet to a dominant institutional asset class has been remarkably rapid. Understanding this history matters, because it reveals the forces that are likely to shape the next decade.

The 1950s–1980s: The Mainframe Era

The first “data centres” were simply temperature-controlled rooms housing massive mainframe computers, owned and operated by large corporations and government agencies. IBM, Burroughs, and GE built the machines; their clients built the rooms. There was no network connectivity, no sharing of resources. Each facility was an island.

The 1990s: The Dot-Com Boom and the Birth of Colocation

The commercial internet created a need for neutral interconnection points — places where different networks could exchange traffic. In 1998, Al Avery and Jay Adelson founded Equinix in Ashburn, Virginia, with a simple idea: build a facility where competing networks could connect on neutral ground. That idea became the foundation of the modern colocation industry, where multiple tenants share a single facility.

The 2000s: The Rise of the Cloud

The launch of Amazon Web Services in 2006 marked a paradigm shift. For the first time, companies could rent computing power on demand rather than building their own infrastructure. This sparked the explosive growth of hyperscale cloud data centres and began the consolidation of computing power into the hands of a few tech giants.

The 2010s: The REIT-ification of Data Centres

As the market matured, data centres began to be recognised as a legitimate real estate asset class. Equinix converted to a Real Estate Investment Trust (REIT) — a tax-efficient structure that requires the company to distribute at least 90% of taxable income to shareholders — in 2015, followed by Digital Realty and others. This opened the door for a new wave of institutional capital and gave individual investors their first easy access point.

The 2020s: The AI Supercycle

The launch of ChatGPT in late 2022 triggered an arms race for AI dominance. Suddenly, every major technology company needed vastly more computing power than anyone had anticipated. AI workloads represented about 25% of data centre demand in 2025; by 2030, they are expected to account for half. This has kicked off what JLL calls an “infrastructure investment supercycle,” with total data centre expenditures — including construction, fit-out, and tenant equipment — expected to approach $3 trillion by 2030.[1]

| Year | Milestone | Significance |

|---|---|---|

| 1998 | Equinix founded | Birth of neutral colocation |

| 2006 | AWS launches | Cloud computing begins |

| 2015 | Equinix converts to REIT | Data centres become a real estate asset class |

| 2017 | Equinix acquires 29 Verizon data centres for $3.6B | Major consolidation wave begins |

| 2021 | Blackstone takes QTS private for $10B | Private equity enters at scale |

| 2022 | KKR and GIP acquire CyrusOne for $15B | Valuations accelerate |

| 2024 | Blackstone acquires AirTrunk for A$24B ($16.1B) | Asia-Pacific becomes a battleground |

| 2025 | Aligned Data Centers sold for $40B | Largest data centre deal in history |

| 2025 | Data centre M&A hits record $61B | The supercycle is confirmed |

Figure 2: The Data Centre Supercycle — Global Investment Growth (2020–2035E). Source: JLL, company filings.

SECTION III

The Demand Drivers

Three powerful, interlocking forces are driving the demand for data centres to levels that would have seemed absurd even five years ago.

The AI Revolution

AI workloads are extraordinarily power-intensive. A single Nvidia H100 GPU — the chip of choice for training large language models — draws about 700 watts, roughly the same as a microwave oven running continuously. A modern AI training cluster might contain tens of thousands of these chips, packed into racks that draw 40 to 100 kilowatts each, compared to 5 to 10 kilowatts for a traditional server rack. The combined capital expenditure of the four major hyperscalers (Amazon, Microsoft, Google, and Meta) on data centre infrastructure exceeded $200 billion in 2025 and is expected to climb more than 30% in 2026. Amazon alone has committed over $100 billion in AI-focused data centres through 2030.[8]

Cloud Migration

The shift from on-premise corporate data centres to the public cloud continues unabated. Every company that moves its IT infrastructure to AWS, Azure, or Google Cloud is, in effect, transferring its data centre demand to the hyperscalers. This consolidation is a structural tailwind for the largest operators.

Data Growth

The sheer volume of data being created, processed, and stored is growing exponentially. From IoT sensors to streaming video to autonomous vehicles, every digital interaction creates data that needs to live somewhere. Goldman Sachs projects data centre demand to grow roughly 160% to 122 gigawatts by 2030, representing 15% yearly growth between 2023 and 2030.[3]

SECTION IV

The Players

The data centre market is dominated by a handful of powerful players, each with a distinct business model and competitive advantage.

The Hyperscalers

Amazon (AWS), Microsoft (Azure), Google (GCP), and Meta are the four largest consumers and builders of data centre capacity. They both build their own facilities and lease massive amounts of space from third-party operators. Their combined capital expenditure exceeded $200 billion in 2025.

The Public REITs

Equinix is the world’s largest data centre REIT, operating over 260 facilities in 72 metros across 33 countries. Its competitive moat is interconnection — its facilities are the places where networks meet, making them extremely sticky for tenants. Digital Realty is the second-largest, with a portfolio of over 300 facilities globally, focused more on hyperscale leasing.

The Private Equity Giants

Blackstone has become the single largest private owner of data centres in the world, with a portfolio valued at over $70 billion following its acquisition of QTS. KKR, Brookfield, and DigitalBridge are also major players, each with multi-billion-dollar data centre platforms.

| REIT | Ticker | Market Cap | Dividend Yield | Focus |

|---|---|---|---|---|

| Equinix | EQIX | ~$85B | ~2.0% | Interconnection & colocation |

| Digital Realty | DLR | ~$55B | ~2.8% | Hyperscale & colocation |

| Iron Mountain | IRM | ~$35B | ~2.5% | Data centres + storage |

| CyrusOne (KKR) | Private | N/A | N/A | Hyperscale development |

SECTION V

Geography: Where the Data Lives

Data centres are not evenly distributed around the world. Their locations are determined by a complex interplay of factors: proximity to users, access to power, regulatory environment, and climate.

North America

The United States dominates the global data centre market, with Northern Virginia (specifically Ashburn) serving as the world’s largest data centre cluster. The region benefits from a concentration of fibre-optic cables, a favourable regulatory environment, and proximity to the US government and major technology companies. Other key US markets include Dallas, Phoenix, Chicago, and Silicon Valley.

Western Europe

London, Frankfurt, Amsterdam, and Dublin (the “FLAD” markets) are the primary European data centre hubs. Frankfurt benefits from being the financial capital of the eurozone and a major internet exchange point. Amsterdam and Dublin have attracted hyperscalers with favourable tax regimes and access to submarine cables.

The Nordics

Sweden, Norway, and Finland are emerging as attractive locations for data centres due to their cold climates (which reduce cooling costs), abundant renewable energy (primarily hydroelectric), and political stability. Meta and Google have both built major facilities in the region.

Asia-Pacific

Singapore, Tokyo, and Sydney are the primary data centre markets in Asia-Pacific. Singapore imposed a moratorium on new data centre construction from 2019 to 2022 due to power constraints, which has since been partially lifted. Japan is seeing a surge of investment driven by AI demand, with the government actively courting hyperscalers. Blackstone’s $16.1 billion acquisition of AirTrunk in 2024 signalled the growing importance of the region.[4]

Emerging Markets

India, Southeast Asia, and parts of Africa represent the next frontier for data centre development. India’s data centre capacity is expected to triple by 2028, driven by a massive digital population and government initiatives to localise data storage.

SECTION VI

How to Invest in Data Centres

There are several ways to gain exposure to the data centre theme, each with its own risk-return profile and accessibility.

Public REITs

The most accessible route for individual investors. Equinix (EQIX) and Digital Realty (DLR) are the two largest pure-play data centre REITs. Both trade on the NYSE and offer dividend yields of 2-3%. As REITs, they are required to distribute at least 90% of their taxable income to shareholders, providing a steady income stream alongside capital appreciation potential.

| REIT | Ticker | Market Cap | Dividend Yield | Focus |

|---|---|---|---|---|

| Equinix | EQIX | ~$85B | ~2.0% | Interconnection & colocation |

| Digital Realty | DLR | ~$55B | ~2.8% | Hyperscale & colocation |

| Iron Mountain | IRM | ~$35B | ~2.5% | Data centres + storage |

| CyrusOne (KKR) | Private | N/A | N/A | Hyperscale development |

ETFs

For broader exposure, several ETFs provide diversified access to the data centre and digital infrastructure theme. The Global X Data Center & Digital Infrastructure ETF (DTCR) and the Pacer Data & Infrastructure Real Estate ETF (SRVR) are two popular options.

Private Funds

For accredited investors, private equity and infrastructure funds offer the potential for higher returns but with longer lock-up periods and higher minimum investments. Blackstone, KKR, Brookfield, and DigitalBridge all manage dedicated data centre strategies. Minimum investments typically start at $250,000 to $1 million, with lock-up periods of 7-10 years.

FIGURE 3

How a typical private equity data centre deal works — from capital formation through exit.

Capital Formation

LPs commit capital to PE fund

Acquisition

Fund acquires or develops data centre

Operations & Leasing

Stabilise facility, sign hyperscaler tenants

Value Creation

Expand capacity, improve PUE, secure power

Exit

Sell to strategic buyer, another PE fund, or IPO

SECTION VII

Unit Economics: What It Costs to Build and Run a Data Centre

Understanding the unit economics of a data centre is essential for evaluating any investment in the space. The numbers are large, but the margins can be attractive for well-run facilities.

Capital Expenditure (CapEx)

Building a data centre is extraordinarily capital-intensive. A typical hyperscale facility costs between $7 million and $12 million per megawatt (MW) of IT capacity, depending on location, power density, and cooling requirements. A 100MW campus — a mid-sized facility by today’s standards — can cost $700 million to $1.2 billion to build.

| Component | Cost per MW | % of Total |

|---|---|---|

| Land & site preparation | $0.5M–$1.5M | 7–12% |

| Building shell & structure | $1.0M–$2.0M | 14–17% |

| Electrical infrastructure | $2.0M–$3.5M | 28–30% |

| Cooling systems | $1.5M–$2.5M | 21–22% |

| Fire suppression & security | $0.3M–$0.5M | 4–5% |

| Network infrastructure | $0.5M–$1.0M | 7–8% |

| Soft costs (design, permits) | $0.7M–$1.0M | 10–12% |

| Total | $7M–$12M | 100% |

Operating Expenditure (OpEx) — Annual

Once built, data centres have significant ongoing operating costs, dominated by electricity. A 100MW facility can consume $50-80 million in electricity annually, depending on local power rates and the facility’s Power Usage Effectiveness (PUE) — the ratio of total facility energy to IT equipment energy.

| Category | Annual Cost per MW | % of OpEx |

|---|---|---|

| Electricity | $500K–$800K | 55–65% |

| Staffing & management | $80K–$150K | 10–15% |

| Maintenance & repairs | $60K–$100K | 7–10% |

| Insurance | $20K–$40K | 2–4% |

| Property taxes | $30K–$60K | 3–5% |

| Network & connectivity | $40K–$80K | 5–7% |

| Security & compliance | $20K–$40K | 2–4% |

Revenue & Returns

Colocation facilities typically charge $120-$200 per kW per month, while hyperscale leases range from $80-$150 per kW per month on longer-term contracts. Well-operated facilities can achieve EBITDA margins of 50-60%, with stabilised yields on cost of 8-15% depending on the market and lease structure. The combination of high barriers to entry, long-term contracts, and inflation-linked escalators makes data centres an attractive asset class for yield-oriented investors.

SECTION VIII

Macroeconomic Sensitivity

Data centres sit at the intersection of real estate, technology, and energy — making them sensitive to a range of macroeconomic factors.

Interest Rates

As capital-intensive assets, data centres are sensitive to interest rate movements. Higher rates increase the cost of debt financing for new construction and can compress valuations of existing assets. However, the strong demand backdrop and long-term lease structures provide some insulation. The sector performed well through the 2022-2024 rate hiking cycle, suggesting that demand fundamentals can outweigh rate headwinds.

Inflation

Data centres have built-in inflation protection through lease escalators, which typically range from 2-4% annually. Construction costs are sensitive to inflation in materials (steel, copper, concrete) and labour, which can erode development margins. However, the ability to pass through higher costs to tenants on new leases provides a natural hedge.

Energy Prices

Electricity is the single largest operating cost for a data centre. In most colocation arrangements, power costs are passed through to tenants, limiting the operator’s direct exposure. However, in gross lease structures, the operator bears the risk. Rising energy prices can also slow the pace of new development by making projects less economically viable.

Recession Risk

Data centres proved remarkably resilient during the 2020 recession, as the shift to remote work and digital services actually accelerated demand. The essential nature of cloud computing and the long-term contractual commitments of hyperscaler tenants provide significant downside protection. However, a severe recession could slow enterprise cloud migration and reduce discretionary IT spending.

SECTION IX

Tax Considerations

The tax treatment of data centre investments varies significantly depending on the investment vehicle and the investor’s jurisdiction.

REIT Taxation

REIT dividends are generally taxed as ordinary income, not at the lower qualified dividend rate. However, the Tax Cuts and Jobs Act introduced a 20% deduction for qualified REIT dividends through 2025, effectively reducing the top tax rate on REIT income from 37% to 29.6%. This provision has been extended through 2028.

Private Fund Taxation

Private equity data centre investments are typically structured as partnerships, with income flowing through to investors. Capital gains on the sale of assets held for more than one year are taxed at the long-term capital gains rate (currently 20% for high-income investors, plus the 3.8% net investment income tax). Depreciation deductions can provide significant tax benefits in the early years of ownership.

Opportunity Zones

Several major data centre development sites are located in designated Opportunity Zones, which offer significant tax benefits including deferral of capital gains, a step-up in basis, and potential elimination of gains on the Opportunity Zone investment if held for 10 or more years.

International Considerations

For investors considering international data centre exposure, tax treaties, withholding rates, and local tax incentives can significantly impact after-tax returns. Ireland, Luxembourg, and Singapore have historically offered favourable tax regimes for data centre operators, though global minimum tax initiatives (Pillar Two) are beginning to erode some of these advantages.

SECTION X

Case Studies

Case Study 1: Blackstone and QTS — The $10 Billion Bet

In June 2021, Blackstone acquired QTS Realty Trust for $10 billion, taking the data centre REIT private in what was then the largest data centre transaction in history. At the time, some analysts questioned the price — a 21% premium to QTS’s undisturbed share price. By 2025, the QTS portfolio had become the single largest driver of returns across Blackstone’s entire $1.3 trillion asset base.[2] The thesis was simple: AI demand would create a structural shortage of data centre capacity, and QTS’s land bank and power capacity gave it the ability to build at scale. Blackstone invested over $30 billion in expanding the platform, and the portfolio is now valued at more than $70 billion.

Case Study 2: The $40 Billion Aligned Mega-Deal

In 2025, Macquarie Asset Management sold Aligned Data Centers to a consortium for approximately $40 billion — the largest data centre transaction in history, surpassing even the Blackstone/QTS deal.[6] Macquarie had acquired Aligned for a fraction of that price just a few years earlier, generating extraordinary returns for its investors. The deal illustrated both the explosive growth in data centre valuations and the appetite of institutional capital for the asset class.

Case Study 3: The Contrarian — A Billionaire's Warning

Not everyone is bullish. Fernando de Leon, a billionaire data centre developer, warned in December 2025 that the market was overheating. “We are building data centres faster than we can fill them in some markets,” he told CNBC. “The valuations being paid today assume that demand will continue to grow at the current pace for the next decade. That is a dangerous assumption.”[5] De Leon pointed to the growing gap between announced capacity and actual leasing activity in some secondary markets as evidence that the market was getting ahead of itself.

SECTION XI

The Power Problem

The single biggest constraint on data centre growth is not demand, capital, or land — it is power. The electricity required to run the world’s data centres is growing at a pace that is straining power grids and forcing a fundamental rethink of energy infrastructure.

Goldman Sachs estimates that US data centre power demand will grow 160% by 2030, from approximately 47 gigawatts to 122 gigawatts.[3] To put that in perspective, 122 gigawatts is roughly equivalent to the entire electricity consumption of Japan. In Northern Virginia — the world’s largest data centre market — the local utility, Dominion Energy, has warned that it cannot meet the projected demand growth without massive new investment in generation and transmission infrastructure.

The Nuclear Option

Several hyperscalers are turning to nuclear power as a solution. Microsoft signed a 20-year power purchase agreement with Constellation Energy to restart the Three Mile Island nuclear plant. Amazon has invested in small modular reactor (SMR) technology. Google has signed a deal with Kairos Power for SMRs to power its data centres by 2030.

On-Site Generation

Some operators are exploring on-site power generation using natural gas turbines, fuel cells, or even small nuclear reactors. This approach reduces dependence on the grid but adds complexity and regulatory challenges. The trend toward on-site generation is likely to accelerate as grid constraints become more binding.

SECTION XII

Inside a Data Centre: What You're Actually Buying

Amodern data centre is one of the most complex buildings on earth. Understanding what goes into one helps explain why they are so expensive to build and so difficult to replicate.

The core of a data centre is the data hall — a large, climate-controlled room filled with rows of server racks. Each rack holds multiple servers, and each server contains processors, memory, and storage. The racks are arranged in alternating “hot” and “cold” aisles to optimise airflow and cooling efficiency.

Surrounding the data hall is a complex ecosystem of supporting infrastructure: uninterruptible power supplies (UPS) that provide instant backup power in the event of a grid outage; diesel generators that can sustain operations for days if necessary; cooling systems that range from traditional computer room air conditioning (CRAC) units to advanced liquid cooling systems; and fire suppression systems that use inert gases rather than water to protect sensitive equipment.

The Power Usage Effectiveness (PUE) ratio is the industry’s standard measure of energy efficiency. A PUE of 1.0 would mean that all electricity goes directly to computing; in practice, the best facilities achieve PUEs of 1.1-1.2, meaning that for every watt of computing power, only 0.1-0.2 watts are consumed by cooling and other overhead. The industry average is approximately 1.58, according to the Uptime Institute.[7]

SECTION XIII

The Hyperscaler Dilemma: Friend or Foe?

The hyperscalers — Amazon, Microsoft, Google, and Meta — are both the data centre industry’s biggest customers and its biggest potential competitors. This creates a fundamental tension that investors must understand.

On one hand, hyperscaler leasing is the primary driver of demand growth. Their multi-billion-dollar commitments to cloud and AI infrastructure require vast amounts of data centre capacity that they cannot build fast enough on their own. On the other hand, each hyperscaler is also building its own data centres at an unprecedented pace. Amazon alone has committed over $100 billion in data centre investment through 2030.[8]

The key question for investors is whether the hyperscalers will eventually internalise enough capacity to reduce their dependence on third-party operators. The evidence so far suggests that the answer is no — the pace of demand growth is simply too fast for any single company to meet entirely through self-build. But the risk remains, and it is one that investors should monitor closely.

SECTION XIV

Edge Computing: The Next Frontier

While hyperscale data centres dominate the headlines, a quieter revolution is taking place at the edge of the network. Edge computing — processing data closer to where it is generated — is creating a new category of smaller, distributed data centres.

Applications like autonomous vehicles, augmented reality, industrial IoT, and real-time AI inference require ultra-low latency that centralised data centres cannot provide. A self-driving car cannot wait for data to travel to a data centre hundreds of miles away and back — it needs processing power within milliseconds of reach.

Edge data centres are typically much smaller than hyperscale facilities — ranging from a single rack to a few megawatts of capacity — and are located in urban areas, at cell tower bases, or within enterprise campuses. The edge computing market is expected to grow from approximately $60 billion in 2025 to over $230 billion by 2030, creating opportunities for investors who can navigate the fragmented landscape.

SECTION XV

Lessons from History: What Past Infrastructure Booms Tell Us

Every great infrastructure boom in history has followed a similar pattern: a transformative technology creates genuine demand, capital floods in, overbuilding occurs, and a painful correction follows — before the long-term thesis ultimately proves correct.

The Railroad Boom (1840s–1870s)

The parallels between the current data centre boom and the 19th-century railroad boom are striking. Both involved massive capital investment in physical infrastructure to support a transformative technology. The railroad boom ended in the Panic of 1873 and widespread bankruptcies — but the railroads themselves became the backbone of the modern economy.

The Fibre-Optic Boom (1996–2001)

The dot-com era saw massive overinvestment in fibre-optic cable. Companies like Global Crossing and WorldCom laid millions of miles of fibre, much of which went unused for years. The bust was devastating — but the infrastructure they built became the backbone of the modern internet. The lesson: the infrastructure was needed, but the timing and valuations were wrong.

The Shale Oil Revolution (2010–2020)

The US shale oil boom shares several characteristics with the data centre boom: a technological breakthrough (hydraulic fracturing) that unlocked vast new supply, a flood of capital from yield-hungry investors, and a cycle of overbuilding and consolidation. The survivors were the companies with the best assets, the lowest costs, and the most disciplined capital allocation.

SECTION XVI

The Risks

No investment is without risk, and data centres — despite their strong fundamentals — face several significant headwinds that investors must weigh carefully.

Valuation Risk High RISK

Data centre valuations have reached levels that make many experienced real estate investors uncomfortable. Cap rates have compressed to 4-5% for prime assets, compared to 6-8% just five years ago. At these levels, there is limited margin for error.

Power Constraints High RISK

The availability of reliable, affordable power is the single biggest constraint on data centre growth. In key markets like Northern Virginia, lead times for new power connections have stretched to 4-6 years. Operators that cannot secure power will be unable to grow.

Technology Obsolescence Medium RISK

The rapid evolution of AI hardware — from GPUs to custom ASICs to quantum computing — could render current data centre designs obsolete. Facilities built for today’s AI workloads may not be suitable for tomorrow’s, requiring expensive retrofits or replacements.

Concentration Risk Medium RISK

The data centre industry is heavily dependent on a small number of hyperscaler tenants. If any of the major cloud providers were to significantly reduce their leasing activity, the impact on the broader market would be severe.

Regulatory Risk Medium RISK

Governments around the world are increasingly scrutinising the environmental impact of data centres. Water usage, energy consumption, and carbon emissions are all attracting regulatory attention. New regulations could increase operating costs or restrict development in certain markets.

Oversupply Risk Medium RISK

The current wave of construction could lead to oversupply in certain markets, particularly secondary locations where demand is less certain. The history of infrastructure booms suggests that some degree of overbuilding is inevitable.

SECTION XVII

The Alternative Fortune Verdict

So, should you invest in data centres? As with any investment, the answer is not a simple yes or no. It depends on your time horizon, your risk tolerance, and your access to the best opportunities. What we can say with confidence is that data centres are no longer an “alternative” asset class. They are a core component of the modern global economy, as essential as ports, roads, and power grids. The demand for computing power is a structural trend that is likely to persist for decades.

What is clear is that the early, straightforward phase of this market is over. The days of buying a portfolio of data centres and riding the wave of cloud adoption have given way to something more complex — a landscape shaped by the power crunch, rapid technological change, and the blurring line between tenant and owner. The next chapter will reward depth of understanding, not just enthusiasm.

For anyone doing their own due diligence, here are the questions worth asking:

Due Diligence Questions

For Public REITs:

What is the company’s exposure to the hyperscale tenants? How much of its revenue comes from the top 3-4 cloud providers?

What is its interconnection strategy? Does it have a defensible moat based on network effects?

What is its power procurement strategy? Has it secured long-term power contracts at attractive rates?

How old is its portfolio? Will it need to make significant investments to upgrade its facilities for AI workloads?

For Private Funds:

What is the manager’s track record? Have they successfully developed and operated data centres through multiple cycles?

What is their strategy for securing power? Do they have in-house energy expertise?

How are they sourcing deals? Are they finding proprietary opportunities or competing in crowded auctions?

What are the fund’s terms? What are the fees, the carry, and the lock-up period?

The bulls will point to insatiable AI demand, a structural supply shortage, and the most creditworthy tenants on the planet. The bears will point to eye-watering valuations, a power grid that cannot keep up, and a history of infrastructure booms that ended in tears before they ended in transformation. Both sides have the data to make their case. The job of this deep dive was to give you all of it — so the conclusion you reach is your own.

PREVIOUS ISSUE

Private Credit: The $3.5 Trillion Shadow Banking System Reshaping How Wealth Is Built

A comprehensive analysis of the eight pillars of private credit, the players who control it, and whether it belongs in your portfolio.

THE FORTUNE CLUB

Go Deeper With Our Community

Fortune Club members get access to model portfolios, live Q&A sessions with alternative investment managers, our private investor community, and exclusive deep-dive supplements with specific fund recommendations.